It’s been a couple of years since I have written a blog post on the YLS Cost of Living survey and felt it was time to re-address what it is we actually do with this survey data and why it’s critical to the financial aid process. And along the way I will share some of the specific results of the recently completed 2014-2015 survey.

WE CAN’T DO IT WITHOUT YOU– the Cost of Living survey is only valuable when students take the time to respond and provide accurate data. So thank you to everyone who completed our 14-15 survey which yielded a 32% response rate of all YLS JD and Graduate students ( down from the 13-14 year response rate of 42% but still yields a good enough sample to draw conclusions.)

WHAT DOES ANY OF THIS HAVE TO DO WITH FINANCIAL AID? In order to award aid (by federal regulations) we must annually develop a “Cost of Attendance” (i.e. budget) which represents both the fixed (think tuition and fees) and estimated (i.e. books, housing, food) costs that a student attending YLS would incur. . That Cost of Attendance forms that basis of all aid awards since the need based aid formula is Cost of Attendance – Contribution (student, parent etc.) = Need. So to come up with those estimated costs of books, housing, food etc. we go (through the survey) to the people actually incurring these costs- our students- .

WHY FOCUS THE SURVEY ON ONLY CERTAIN EXPENSES? – The Department of Education regulations specify what are “allowable” expenses in the Cost of Attendance and it’s usually a pretty narrow definition. They also mandate that the same Cost of Attendance must be used for all students in the same degree program So we can’t create budgets based on each individual student’s spending pattern or needs… everyone is held to same overall Cost of Attendance accountability.

THE “BONUS”- beyond helping us build the Cost of Attendance, the survey gives us information to evaluate financial challenges among our students, which we can then address. . For example the increasing cost of professional clothing in last year’s survey led to our “Dress For Success For Less Workshop” this past year, as well as our increasing the COAP eligible suit loan from $350–$600.

SO… WHAT DID THE SURVEY SAY…? Some highlights (in a geeky “I love data” kind of way):

99% of our students live in New Haven – that figure is not much different than in prior years but this year we added a question asking in what area or neighborhood :

Where YLS Students live in New Haven

| Downtown |

61%

|

| East Rock |

26%

|

| West River |

0%

|

| Westville |

1%

|

| Wooster Square |

5%

|

| Other |

7%

|

So the pragmatist in me says it makes sense that people want to live in downtown as close to YLS as possible. But the Financial Aid Director in me looks at that same data and worries about the “price” of that convenience given that Downtown rents are notoriously higher priced.

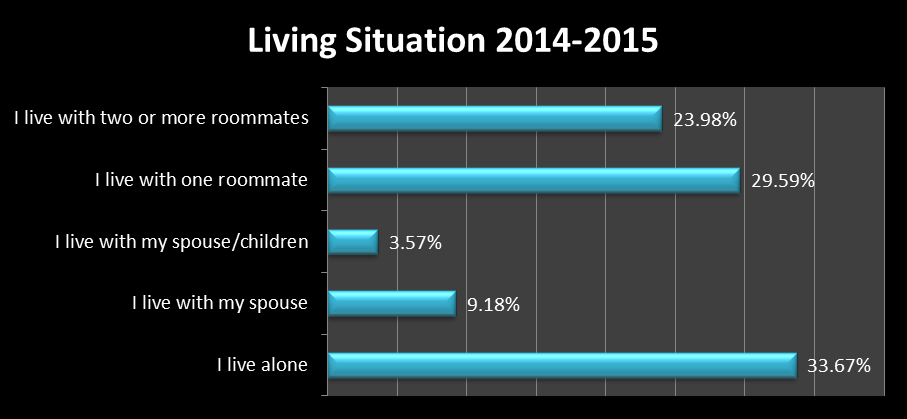

Living Situation data on the whole differed very little from the 13-14 year but when we drill down a little into this data and start segmenting it by class year … we find a very interesting development:

| |

Class Year

|

|

1L

|

2L

|

3L

|

Graduate

|

|

I live alone

|

32%

|

36%

|

24%

|

57%

|

|

I live with my spouse

|

7%

|

6%

|

15%

|

21%

|

|

I live with my spouse/children

|

2%

|

4%

|

6%

|

0.00%

|

|

I live with one roommate

|

35%

|

25%

|

32%

|

14%

|

|

I live with two or more roommates

|

23%

|

28%

|

24%

|

7%

|

For the first time (in the 5 years that I have been conducting the survey) – the percentage of 1Ls living with roommates surpassed the number of 1Ls living alone. To me that’s a very positive trend because there are huge cost savings in living with roommates (and even more if you can do it for all three years). How much savings?

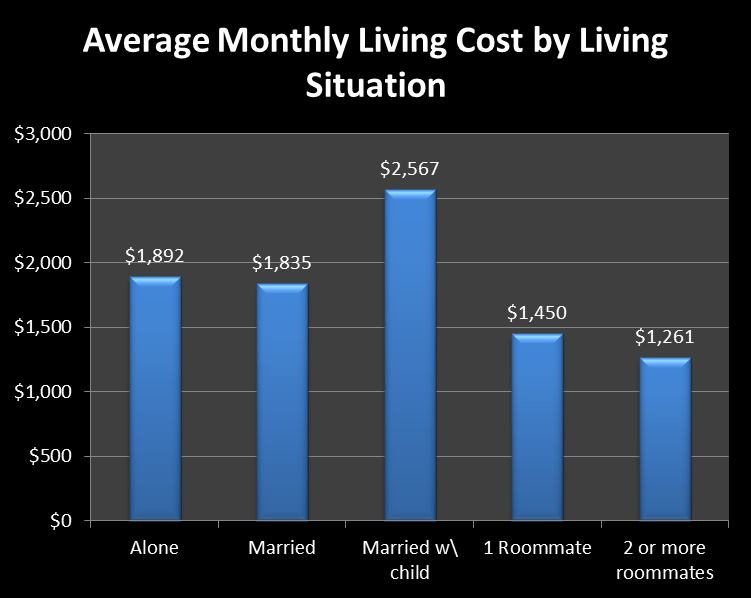

Our survey answers that as well:

Let’s do the math – that cost difference between living with a roommate (let alone two or more roommates) is $3,978 for the 9 month academic year. If you lived alone for all three years that’s $11,394. Think that’s a lot? How about if you had to borrow that amount in extra Grad Plus loan funds and then pay it back on a 10 year repayment- total cost then for wanting to live alone for your three years of law school is now – $16,230?

The Average Monthly Living Cost decreased from 13-14 (primarily due to a drop in the average rent/housing cost) and given that data it’s awfully hard to justify an increase to the present $17,000 allotted for living in the student budget.

| EXPENSE CATEGORY |

2013-2104 |

2014-2015 |

| Rent/mortgage* |

$921 |

$891 |

| Basic Household utilities |

$92 |

$91 |

| Telephone (cell or landline) |

$69 |

$67 |

| Cable/Internet |

$51 |

$46 |

| Food |

$443 |

$432 |

| Local Transportation |

$142 |

$105 |

| Average Monthly Total: |

$1,718 |

$1,631 |

| Academic Year Total (9 months) |

$15,461 |

$14,679 |

In addition, the present estimate of $1,100 for books is fairly accurate given that the survey showed 2Ls and 3Ls spending an average of $954 last academic year.

THINGS THAT WORRIED ME:

- A higher percentage (28%) of students indicate they primarily get their meals by “eating out-“ than last year (17%) with a corresponding decrease in students who make meals at home (77% to 56% ). As a wise, former YLS student so eloquently shared with me “buying meals out is one of the most efficient ways to deplete your budget”. ( A quote I should have carved over our office entrance)

- There were some “ongoing” expenses cited for which we can make budget adjustments and allow additional COAP eligible loan borrowing- professional clothing, travel for Clerkship interviews and computer purchases. I worry from the responses that not everyone knew this option was available to them.

- Many people cited out of pocket health costs as a challenge. Per federal regulations this is an area where on an individual case by case basis we can potentially make a budget adjustment for additional loan funds (however not COAP eligible) but in a cash flow situation that might help you deal with these costs. If this is your situation, come talk to us.

- Of all the responses to “what are other ongoing expenses not captured elsewhere on the survey”- the most common was “gifts” for the holidays, for weddings, for birthdays etc. I know this is going to sound preachy but I need to say it.. the fact that you are here at Yale Law School has to make your family and friends very happy and proud. I think they would understand that for three very short years of your life you are going to be facing some financial constraints and restrictions that may hinder your ability to give pricey gifts. But you should never forget that the biggest/best gift for them will be your graduation from YLS. Seriously the only “wedding gift” that I received and still use on a daily basis is a very inexpensive hand crafted piece of pottery and I have never used one place setting of my Lenox china. I’m just saying… people will understand your situation

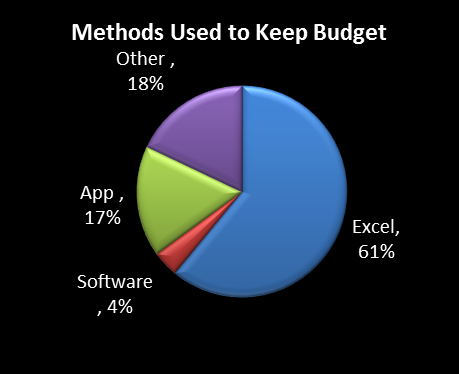

SOMETHING THAT MADE ME HAPPY:

57% of you indicated that you keep a budget!!! That’s the key to this whole Cost of Attendance challenge. And interestingly most of you are keeping it on a basic Excel spreadsheet and if using an app or software the majority are using mint.com If you are not keeping a budget you may want to check out the basic excel budget template we have available on the Inside Page.

THE BOTTOM LINE: As with all things financial- we have to end with the bottom line… we will retain the $17,000 allowance for “living” and $1,100 allowance for “books” in next year’s 2015-2016 Cost Of Attendance because based on the survey data (which is the only empirical evidence we have) an increase is not justified. That $17,000 allowance is still above the $14,679 average academic year living costs calculated by the survey and, as such ,we are still allowing a $2,321 “buffer” for higher cost choices or to cover some of the ancillary costs. (toiletries, household expenses, entertainment, technology maintenance, pet care, etc.) cited as ongoing expenses in the survey. We also need to point out that increasing the “living allowance and Cost of Attendance in general also increases the amount of unit loans offered to you and your overall borrowing/debt.

So my best advice is:

1) Start/continue to keep a budget so that you can live within that allowance, recognizing the reality that while here (again for three short years) you are going to need to make some challenging financial choices, decisions and sacrifices

2) Don’t hesitate to come to the Financial Aid Office to discuss any of the financial challenges that you face. There are circumstances under which we can make aid adjustment and, at the very least, we may be able to offer support and help you come up with some creative solutions.