Laying Down The Law… On The Results Of Our 2015-2016 Cost of Living Survey

Every year I write a blog post with the outcome of the COL survey and I am always trying to think of a new way to deliver these results. For this year I decided to focus on something near and dear to all of you… the “Law” (or rather the law behind “why” we do the survey).

The Cost of Attendance (aka “student budget”) that is the basis of our financial aid award system is determined by the Higher Education Act of 1965 (Sec. 472 ). And while that law specifically details what types of costs are and are not allowed to be included in the Cost of Attendance, it puts the onus on the school to determine the “appropriate and reasonable” amounts for each cost. The Act specifies that:

- You can include an “allowance” for room and board for those living off campus but it “must be based on reasonable expenses for the student’s room and board “

- An allowance can also be included for “books, supplies, transportation and miscellaneous personal expenses”. And again it’s vaguely quantified as a “reasonable amount” as determined by the school.

The challenge of the Act is that it then dictates that “students must be awarded on the basis of a Cost of Attendance comprised of allowable costs assessed all students carrying the same academic workload. “. You need to use a common Cost of Attendance for every student in the same degree program in determining aid. In other words, there cannot be individual budgets based on each student’s actual costs incurred or on lifestyle choices students may make.

So the annual survey is born out of our need to judiciously establish that level of “appropriate and reasonable” for room and board, transportation and book expenses and then calculate “average costs” that we feel can be applied to all students.

Here is what we learned from this year’s survey:

- First off, we had an excellent response rate of almost 40% of all JDs and Graduate students. So the data collected is from a good representative sampling of students. Thank you to all who took the time to complete the survey.

- As in past years, the vast majority of students choose to live in New Haven (97%) with 61% indicating they chose to live in “downtown” New Haven followed by 26% in East Rock.

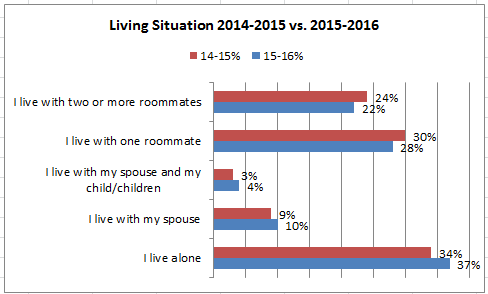

- We saw an uptick in the number of students living alone versus living with a roommate. And that trend increased in all JD classes (1Ls-3Ls).

It’s what drove us to actually do a short supplemental survey targeted to anyone who was living alone to understand this choice better. The most wide spread answers as to “why” people were living alone were : the need for personal space to study/work, the inconvenience/ challenge of sharing space and a desire for independence/freedom. All valid personal reasons for making this choice- but a recognized “choice” (not necessity) none the less.

It’s what drove us to actually do a short supplemental survey targeted to anyone who was living alone to understand this choice better. The most wide spread answers as to “why” people were living alone were : the need for personal space to study/work, the inconvenience/ challenge of sharing space and a desire for independence/freedom. All valid personal reasons for making this choice- but a recognized “choice” (not necessity) none the less.

Should additional financial aid be allocated to support that personal choice? That’s a tough judgment to make given that by law the budget must be “reasonable” and apply across the board to all students in the same degree program.

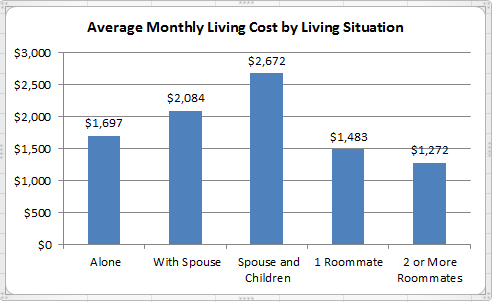

But what concerns me most is the long term cost of that choice. Based on the average inclusive monthly living costs (more detail on that later) here is the comparison between all the living arrangements.

So let’s look at it this way… monthly difference between living alone ($1,697) vs. living with two or more roommates ($1,272) is $425/month. For the nine month academic year that’s $3,825 or for a three year JD degree it’s $11,475. If you’re paying for that higher cost by borrowing Grad Plus loans then you’ve got interest building on that $11,475 so that by the time it goes into repayment it’s now… $15,000. If you go on a 10 year repayment plan then ultimately (with interest) you are paying off a balance of $20,899 or (worse) on a 25 year plan $31,805. That’s what choosing to live alone is actually costing you- and it’s a pretty high price for solitude.

So let’s look at it this way… monthly difference between living alone ($1,697) vs. living with two or more roommates ($1,272) is $425/month. For the nine month academic year that’s $3,825 or for a three year JD degree it’s $11,475. If you’re paying for that higher cost by borrowing Grad Plus loans then you’ve got interest building on that $11,475 so that by the time it goes into repayment it’s now… $15,000. If you go on a 10 year repayment plan then ultimately (with interest) you are paying off a balance of $20,899 or (worse) on a 25 year plan $31,805. That’s what choosing to live alone is actually costing you- and it’s a pretty high price for solitude.

The key data from the survey is the average cost per month calculation. We “bundle” the responses to several of the questions to come up with that average. For 2015-2016 it came out to:

That $15,435 is a 5% increase over last year’s average of $14,679. But it’s still well below the $17,000 that we have been budgeting for living expenses.

Other takeaways from the survey data:

- 40% of you continue to purchase food “out” or from the YLS Dining Hall. I know for the sake of convenience and your busy schedules that’s the easiest options but cannot stress enough how making a couple of meal per week at home or brown bagging your lunch each day can save you considerable dollars.

- Average annual cost for books was $782- so the $1,100 we budget should support that.

- Average cost of professional clothes increased by 3% to $673 per year. So our $500 allotment for the COAP eligible suit loan falls a little short there and will be examined.

- 54% of you indicated you “keep a budget”. I love hearing that but wish we could have seen a significant bump up in that number this year. Again if you have any questions on setting up a budget, need a good Excel template to follow, want to know what aps are good to use etc., come by our office.

- Several surveys cited that the YLS living allocation was less than other Yale Graduate Schools. In actuality, YLS has historically been and continues to be the second highest allocation behind SOM.

- When we asked you to identify any other “ongoing expenses” several people cited support they provide parents or other family members. And while I empathize with your obligation to help and care for your family, financial aid and the student budget are, again by law, meant to support the student only. But if you have a challenging family situation I absolutely encourage you to come discuss it with me so that we can see what other options (within regulations) might help you.

-

Pets= $$$$$. But finally an excuse to put their picture in a blog post!! L to R Buffer, Del and Spats Also in the “ongoing expenses” many of you cited the costs of keeping your pets (specifically a significant number of cat owners). I completely get this one having spent a near fortune on my three cats on veterinary bills, cat food and, of course, enabling their catnip “habit”. As an animal lover, if it were up to me, I would classify them as “dependents” but again based on those federal regulations- no such luck for a student budget.

So what does it all mean for you? For the 2016-2017 academic year we are going to maintain a book allowance of $1,100 and a general living allowance of $17,000 (particularly since based on the average monthly cost that would still grant a $1,565 buffer between the $15,435 average per year vs. the $17,000 presently allocated). That buffer is there to support incidentals, household expenses, higher cost travel and emergencies that many of you cited in the survey as “additional costs”.

We want our financial aid calculations to be a transparent and public process. So if you have additional questions on the Cost of Living survey, its use or how aid awards are made, please reach out to our office and we would be happy to explain or run a mock aid award for next year for you. Also if you are challenged to stretch your funds to meet costs or are seeking ways to maintain a budget, we are always here to offer advise and resources in that regard also.